How much will I need to retire?

The ‘Bengen Rule’, also known as the ‘SAFEMAX rate’ or, more popularly, as the ‘four percent rule’ suggests that those who only take up to 4 percent* from their portfolio in their first year of retirement, and adjust that amount for inflation in subsequent years, stand a greater chance their wealth will outlive them.

Using the four percent rule as a rule of thumb then, if you want a pension of €40,000 Euro in your first year of retirement you’ll need a pension pot of €1 million (€1 million x 4% = €40,000).

By reversing the maths, we can also use the four percent rule to calculate the pension pot you’ll need by using 25 x your-annual-spending. So, if you spend €100,000 a year, you’ll need a retirement investment of €100,000 x 25 = €2.5 million, but, if you’re planning to spend only €50,000 in the first year post-retirement, then you’re investment needs to be €1.25 million.

Using Bengen’s research, the four percent rule suggests that, if you invest in a balanced portfolio you should be able to withdraw 4 percent of your investment during the first year and then, adjusted for inflation, every year for thirty years of retirement without running out of money.

The four percent rule is, however, only meant as a guideline. It assumes an investment portfolio evenly split between stocks and bonds, a market with regular peaks and troughs, and average economic conditions. The rule merely gives you an idea of what your retirement needs might be; in William Bengen’s own words to the New York Times, “I always warned people that the 4 percent rule is not a law of nature like Newton’s law of motion. It is entirely possible that at some time in the future there could be a worse case”.

One thing, however, is as certain as certain gets; the earlier you start saving, and the more you save, the better off you’ll be because, after all, every penny helps!

What should I save for retirement?

The chart below shows how much you would need to save each month starting from different age points to retire with an investment of €1 million.

Of course, when it comes to planning your retirement and how you intend to fund it, the over-riding factor is all down to determining the lifestyle you want to have when you retire and the lifestyle you have pre-retirement. What you spend now, what you intend to spend in retirement, and what you want to leave as an inheritance, all have direct correlations to what you save now.

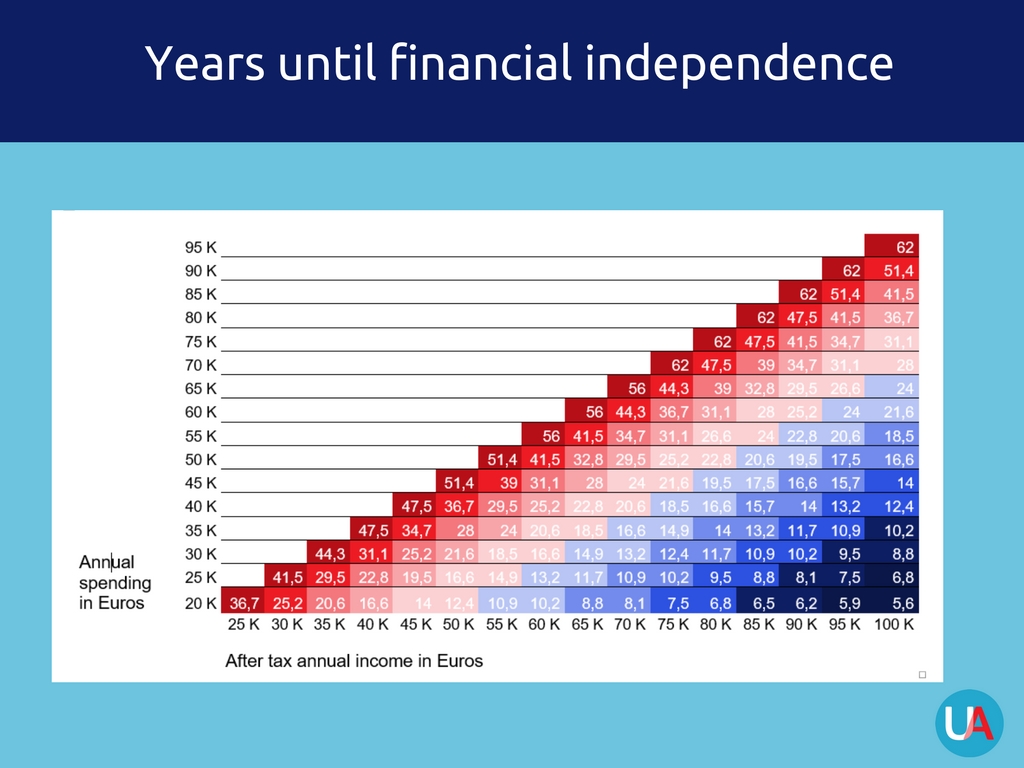

Inevitably, how much you can afford to save very much depends on the difference between how much you earn and how much you spend; you so-called ‘disposable income’. By comparing income against expenditure and, assuming you save your ‘disposable income’, the chart determines how long you would need to save before you can retire. The chart assumes no existing savings, an annual withdrawal rate of 4% once you retire, and an annual investment return of 5%.

If you’d like to talk with someone about saving for your future and designing a financial plan around your lifestyle, so that you can have the kind of life you want when you retire, please contact us now.

*Revised 2006 to 4.1% (taxable) and 4.5% (tax free)